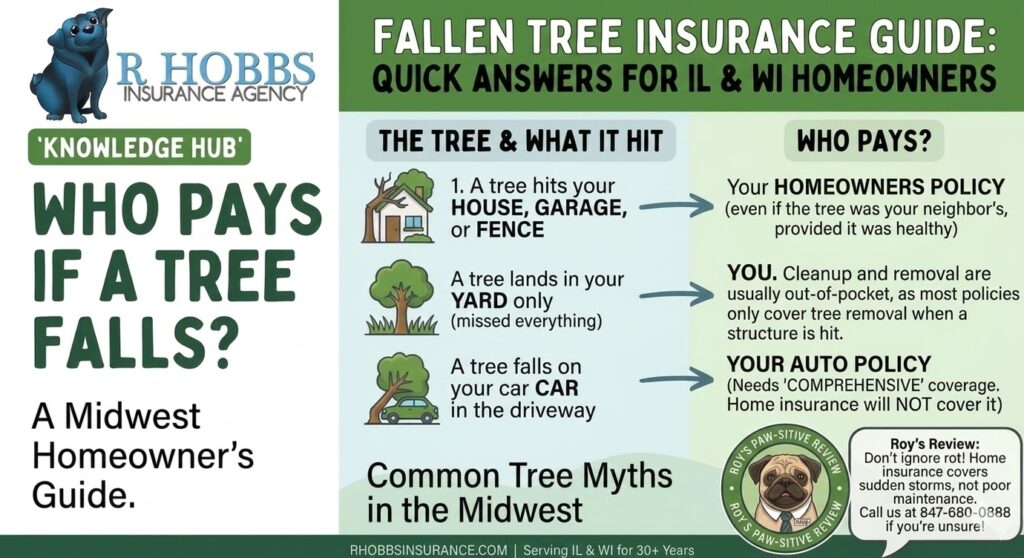

The Quick Answer: Generally, yes—if a tree falls on your house, garage, or fence due to a “covered peril” (like wind, hail, or lightning), your homeowners insurance pays to repair the damage. However, if the tree falls in your yard without hitting anything, you are usually responsible for the cleanup costs yourself.

Who pays if my neighbor’s tree falls on my house?

This is a common question we get in Lincolnshire after a big storm. In most cases, you file the claim with your own insurance company. Even if the tree lived in your neighbor’s yard, insurance follows the property that was damaged. If your neighbor’s tree was healthy and fell due to wind, lightning or a massive windstorm, your policy covers your home.

The Exception: If the tree was dead, rotting, or clearly neglected, your insurance company might try to get your neighbor (or their insurance) to pay. This is called subrogation.

Does insurance pay for tree removal?

This is where it gets tricky for homeowners:

- If it hits a structure: Your policy usually covers the cost to remove the tree from the roof or fence so repairs can begin. This is often capped at $500 to $1,000.

- If it just lands in the grass: Most policies will not pay to haul the tree away.

- The Driveway Rule: Some policies will cover removal if the tree is blocking your driveway or a handicap-accessible ramp, even if it didn’t hit the house.

Common “Tree Myths” in Illinois & Wisconsin

- Myth: “My car is covered by my home insurance if a tree falls on it in my driveway.”

- Reality: No. You would need Comprehensive Coverage on your auto insurance policy to cover a tree falling on your vehicle.

- Myth: “I can claim my prize oak tree if it dies from old age.”

- Reality: Insurance covers “sudden and accidental” damage. Maintenance, rot, and old age are the homeowner’s responsibility.

Pro-Tip from Lynn & Chris: The “Pre-Storm” Check

In the Midwest, we see everything from heavy ice loads to summer “derecho” winds. To avoid a claim altogether:

- Check for “Target Hazards”: Look for dead limbs hanging over your roof or power lines.

- Document Property: Take a quick video of your yard and roof today. Having “Before” photos makes the “After” claim process much faster.

- Check your Deductible: Remember, you have to pay your deductible first. If a tree does $1,200 in damage and your deductible is $1,000, it might be better to pay for the repair out of pocket to keep your claims history clean.